Energy is back in the headlines in a way not seen since the 1970s. Europes reliance on natural gas from Russia is under increased scrutiny because of the ongoing turmoil in Ukraine.

China recently signed a multiyear, multibillion-dollar gas deal with Russia that underlines the strengthened economic and political cooperation between the two neighbors. Meanwhile, the United States is at the epicenter of a shale oil and gas revolution that is transforming domestic as well as global energy markets and politics. Yet while perhaps less noticed, the energy-based relationships that the United States and China each have with Venezuela—and the interactions among those three countries—have geopolitical implications that are particularly pressing.

Venezuela has the world’s largest proven oil reserves, more than Saudi Arabia, more even than Iran and Iraq combined. The United States and China are the world’s two largest economies, the two largest global oil importers, and Venezuela’s two most important oil partners. Combined, China and the United States consumed more than half of Venezuela’s total oil exports in 2013.

Venezuela’s oil, however, is special: it is “extra-heavy,” meaning that it is particularly carbon-rich, so its development carries greater financial and environmental costs than other types of oil. Venezuela is special in other ways as well; despite the country’s vast energy resources, it is mired in profound economic and social problems, both of which are tied to a deeply polarized political system.

The nature of Venezuelan oil and politics therefore presents the United States and China with significant policy challenges. But such challenges are also opportunities for Washington and Beijing to work together to mitigate the climate impacts of extra-heavy oil, from Venezuela and elsewhere.

For now, U.S. and Chinese government and business leaders are moving in opposite directions in their relations with Caracas. Amid frosty diplomatic ties, the United States is importing less and less Venezuelan oil, while China is accessing, and financing, more and more.

Going forward, the three-way relationship will provide a crucial test of how Washington and Beijing interact as they adopt policies for the use of extra-heavy oils, and for engaging with energy-rich but troubled countries in each other’s near abroad.

Venezuela and Oil: So Much Potential, So Many Problems

A founding member of the Organization of Petroleum Exporting Countries (OPEC), Venezuela has long been a major oil producer. Yet it was only in 2011, after former president Hugo Chávez sponsored the Magna Reserve Project to survey the oil belt in the Orinoco River valley, that the country’s proven reserves reached the number-one global ranking. The Orinoco’s estimated 1 trillion barrels of oil—of which 380–650 billion barrels are technically recoverable today—give Venezuela more proven oil reserves than any other country.

Despite this bounty, Venezuela has been struggling with serious and worsening production woes. According to the International Energy Agency, Venezuela ranks as only the world’s twelfth-largest petroleum producer and ninth-largest exporter, with production falling from a peak of around 3.5 million barrels per day (mbpd) in 1997 to recent lows of less than 2.5 mbpd—the lowest production levels in OPEC.1

Further complicating Venezuela’s energy landscape, the oil in the Orinoco basin is not the typical conventional crude that flows freely out of wells. The Orinoco reserves primarily consist of extra-heavy oil and bitumen, which average an extremely low 8.5° API gravity (the more carbon heavy the oil, the lower the API gravity). This means that the majority of Venezuela’s rich Orinoco reserves will be more costly to extract, transport, and refine—and have a much larger carbon footprint—than most other global oils.

For Venezuela, the gap between its potential and its increasingly troubled petroleum reality is both a sign and symptom of the deeper economic, social, and political problems facing the country. In the mid-1990s, Petróleos de Venezuela S.A. (PDVSA) was generally thought to be the best-run national oil company in the Americas, if not the world. But by the early 2000s, all of that had changed, as Chávez thoroughly restructured PDVSA, turning it into a political tool of his own Bolivarian socialist project and consequently undermining much of the company’s managerial and productive capabilities.

Despite PDVSA’s decreasing productivity, high sustained global oil prices throughout the 2000s gave Chávez unprecedented resources to radically restructure domestic Venezuelan politics and to build a leftist, and largely anti-American, regional Andean and Caribbean foreign policy. However, even before Chávez’s cancer was disclosed in 2011, Venezuela began to experience rising rates of inflation, violent crime, and shortages of consumer goods, as well as deepening social and political polarization. While global oil prices have remained high, all of these problems have only become worse since Chávez passed away in early 2013. Still accounting for around 95 percent of national export earnings and close to 50 percent of overall government revenues, oil remains the problematic foundation of the Venezuelan economy. And oil sales to the United States have long been a key source of support for that structure.

The Declining U.S.-Venezuela Oil Relationship

The United States and Venezuela have had deep, if often conflicted, oil ties for decades. For much of the period since Venezuela first became a major producer and exporter of oil around one hundred years ago, the United States has been Venezuela’s most important oil trade and investment partner. By the mid-1990s, Venezuela had become the largest source of U.S. oil imports, accounting for around 20 percent of the total U.S. import basket (or around 2.1 mbpd). Meanwhile, exports to the United States constituted a majority of Venezuela’s total oil exports.

U.S. Gulf Coast refineries in Louisiana and Texas have adapted to the technical requirements of the relatively heavy and acidic Venezuelan (as well as Mexican) oils. One key byproduct of Gulf Coast refining of extra-heavy Venezuelan oil is petroleum coke, or petcoke, a carbon-rich coal substitute that is removed during upgrading. When burned, petcoke emits high levels of greenhouse gases, comparable to coal, but with more ash and toxic metals. And it is increasingly exported from U.S. refineries to Asia, including China, for use in power generation and industrial production.

At the same time, Citgo, PDVSA’s U.S. commercial arm, has long provided Venezuela with a major refining and gasoline retailing presence in the U.S. petroleum market, which is not only the largest in the Western hemisphere but in the world.

International oil firms had largely been prohibited from investing in Venezuela since the oil industry was nationalized in 1976. But in the mid-1990s, U.S. oil majors like Exxon, Chevron, and Conoco made substantial investments in the country in response to the oil apertura, or opening, in the years before Chávez became president in 1999.

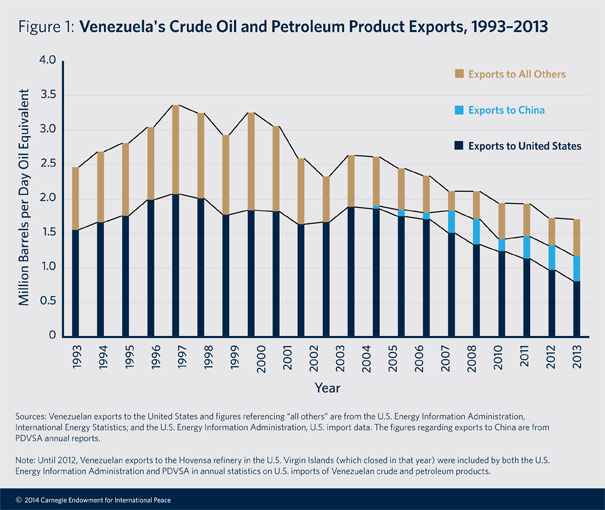

Since peaking in the 1990s, oil trade and investment, not to mention political relations, between Venezuela and the United States have cooled significantly. In 2013, Venezuela was still the United States’ fourth-largest source of crude oil and petroleum product imports, yet at less than 800,000 bpd, Venezuela’s share of U.S. imports had fallen to under 10 percent of the total (see figure below).

Reductions in U.S. imports of Venezuelan oil are largely the result of domestic economic circumstances, broad market forces, and company-specific decisions. One cause of the trend is the recent recession in the United States, which has led to lower gasoline demand and reduced oil imports. Another may be the rapid development of domestic shale oil resources in the United States, but growing domestic supplies have largely affected imports of lighter African crudes rather than heavier oils. The downward trend is also the product of declining Venezuelan production and its replacement in U.S. refineries with oil from Canada’s Alberta oil sands (Canada is now the United States’ number-one source of imports).

Many of the U.S. oil majors (with the significant exception of Chevron) have minimized or abandoned their Venezuelan investments of the 1990s. Companies like Exxon Mobil and ConocoPhillips both dramatically reduced their Venezuela operations after Chávez instituted new rules providing PDVSA with a 60 percent minimum share in all Orinoco joint ventures. Ongoing legal disputes between these U.S. oil majors and the Venezuelan government continue to work their way through international courts, threatening to exacerbate Venezuela’s already precarious debt obligations.

At the same time, Citgo has been refining and selling less Venezuelan oil in the United States, a product of both internal financial difficulties as well as increasing U.S. government dissatisfaction with Chávez and his successor, Nicolás Maduro. Indeed, Venezuelan authorities have been discussing the possibility of selling Citgo, which would likely indicate further reductions in the volume of Venezuelan oil imported into the United States.

In another sign of just how the tables have turned, in 2013, oil-rich Venezuela was importing an unprecedented amount of refined petroleum products from the United States. This highlights the contrast between the booming U.S. domestic oil sector and Venezuela’s increasingly hamstrung one.

Under Chávez and now Maduro, Venezuela has made a public relations display of its efforts to move away from reliance on exports to the United States and to diversify toward Asian partners (primarily China and India). Nonetheless, in 2013 Venezuela still sold around 40 percent of its oil exports to the United States. Thus even as the United States becomes less and less reliant on Venezuelan oil, Venezuela continues to rely on the United States as the largest single export market for its most valuable commodity.

China and Venezuela’s Struggling Strategic Partnership

China’s engagement with Venezuela is of a much more recent vintage than U.S.-Venezuela links, with official ties dating to 1974. Like China’s relations elsewhere in Latin America, its presence in Venezuela has been energized by surging demand for natural resources. Shortly after becoming a net oil importer in the early 1990s, China began to seek out trade and investment opportunities in Venezuela’s oil sector.

However, it was only after Chávez became president that China-Venezuela ties began to flourish into a special kind of bilateral relationship, with China designating Venezuela a “comprehensive strategic partner” in summer 2014. Over a very short period, Chinese oil interests in Venezuela have taken on a form, scale, and importance unmatched by China’s energy and state-to-state relations elsewhere in Latin America. And Chinese imports of Venezuela’s extra-heavy oil or coal-like products such as Orimulsion or petcoke pose clear detrimental climate impacts.

In theory, Venezuela’s unrivaled petroleum supplies are a perfect fit for China’s huge energy demand. While Venezuela’s oil exports to the United States have been falling, those to China have been rising (see figure above). Beginning at under 50,000 bpd of reported crude exports in the mid-2000s, Venezuelan shipments of crude oil to China grew to an estimated 300,000 bpd in 2013 (ranking Venezuela as China’s seventh-largest source of oil imports). These 2013 imports constituted around 5.5 percent of China’s overall crude oil imports and about 15 percent of Venezuela’s overall crude exports.

Moreover, since 2007, China has become Venezuela’s primary source of foreign financing through loans-for-oil deals worth upwards of $50 billion, primarily underwritten by the China Development Bank (CDB). The loans are meant to provide China with preferential, long-term access to Venezuelan crude and petroleum products (in particular fuel oil). In turn, Venezuela has been able to tap into China’s vast pool of state credit even as it has been cut off from many other sources of international finance. At the same time, China’s national oil companies, including the China National Petroleum Corporation (CNPC) and Sinopec, have been key players in Venezuela’s expanding Orinoco exploration and production.

Despite this special China-Venezuela relationship, Chinese government and business leaders have long found Venezuela a frustrating partner. At a general level, expectations have not been met. Even as the two sides have touted vastly expanded oil trade and investment links, China has seen that expansion stymied by both PDVSA’s dysfunctions and Venezuela’s deepening overall economic malaise.

Both Venezuelan and Chinese officials dutifully proclaim, year in and year out, that their trade figures will soon be double or even triple the highest volume ever reached. For instance, PDVSA’s recently fired president, Rafael Ramírez, frequently cited targets of up to 1 mbpd. However, these targets have never been close to being reached.

Although CNPC and Sinopec have inked a number of joint ventures for Orinoco exploration and production, actual production and investments with PDVSA have also been far below stated expectations. The two companies have confronted practical difficulties in their efforts, particularly in terms of upgrading and refining investment and cooperation. In one early indication of those challenges, PDVSA abandoned a large-scale joint project to develop Orimulsion, a patented, majority-bitumen fuel for which Chinese power plants were being refitted. Without fully consulting its Chinese partners, PDVSA decided that the plan was not economically viable and made a unilateral decision to find other market options for the country’s extra-heavy Orinoco crude.

Venezuela’s polarized political system and worsening economic and social problems have come to be seen in China as clear warning signs of an increasingly unstable and unreliable partner. Initially, the way in which Chinese state-owned banks and oil companies established their deals with Venezuela was intended to insulate China from political and economic risk. The CDB, the national oil companies, think tank analysts, and some outside observers agreed that the loans-for-oil structure—not to mention state-to-state ties that had been increasingly developed and deepened—were a strong hedge against any possible Venezuelan default or even against a deterioration in overall trade and investment relations. But especially since Chávez died, observers inside and outside of China have become much less sanguine.

Policy Implications

The U.S. market-led reduction in imports of Venezuelan oil and China’s state-led expansion of oil business with Venezuela demonstrate that the two energy-importing giants are moving in different directions. But the United States and China each have compelling reasons to rethink their shorter- and longer-term policies toward Venezuela and its vast extra-heavy petroleum resources.

For China, the rationale for restructuring its engagement strategy is clear. CDB loans-for-oil deals and other state-to-state commitments have failed to create the desired volume of oil trade and investment opportunities. Instead, Beijing and its banks and oil companies appear to be throwing good money after bad.

A new CDB office has opened in Caracas to more carefully supervise Chinese loans and investments. The real challenge for China, however, is that any dramatic improvement in its oil ties with Venezuela relies on wholesale improvements in Venezuelan economic governance and overall political health. But China’s long-standing yet increasingly impractical policy of noninterference in other countries’ domestic affairs makes addressing such questions deeply problematic.

From a U.S. perspective, the primarily firm-led reduction in Venezuelan oil imports has limited exposure to an ideologically hostile energy supplier. Diplomatic ties between the two countries have been severely strained since Chávez became president and have continued to be in poor repair even after his death. Increased imports of even heavier oil from a (sometimes) friendlier Canada have more than made up for decreasing Venezuelan (and Mexican) imports. Yet reduced U.S. dependence on Venezuelan oil neither constitutes an effective and well-thought-out diplomatic strategy toward Venezuela nor equates with a functional energy and climate policy for the still-significant amounts of Venezuelan crude and petroleum products that are consumed or processed in the United States.

As the world’s largest oil consumers and importers, China and the United States have clear opportunities, indeed imperatives, to work together to mitigate the climate impacts of Venezuela’s extra-heavy oil. Such cooperation, which should be part of an expanded U.S.-China global energy governance and security agenda, could include the setting of market mechanisms like carbon pricing and technical collaboration on carbon-rich products derived from the processing of extra-heavy oil, such as petcoke. Any decisions the two countries make about how to regulate the use of Venezuelan and other extra-heavy oil, in particular from Canada, will set precedents for the rest of the world. But failure to cooperate on creating standards and best practices could mean that either China or the United States cedes the initiative to the other or to more general market forces.

At the same time, Venezuela and its vast energy resources present clear challenges for Chinese and U.S. efforts to create what Chinese President Xi Jinping has called a “new type of great power relationship,” one characterized by cooperation rather than confrontation. Indeed, Venezuela, along with countries like Myanmar in Southeast Asia, stands as an important test case for whether U.S. and Chinese “backyard diplomacy” will devolve into a kind of zero-sum quest for influence—or whether the two countries can cooperate to find new regional balances that benefit all involved. Venezuela lies within the United States’ traditional geographic sphere of influence, while China increasingly sees Southeast Asia as its own backyard and legitimate sphere of influence.

China’s rising energy and political ties to Venezuela have coincided with a period of increasingly antagonistic relations between Venezuela and the United States. During this same period, the United States has rededicated itself to prioritizing relations with countries in East and Southeast Asia.

Energy will be at the heart of these shifting balances for the foreseeable future. Despite inevitable pressures to compete—or even the possibility of confrontation—finding new forms of cooperation on energy and climate should be a priority for U.S. and Chinese policymakers.

Notes

1 Statistics about Venezuelan oil are notoriously contested. For instance, PDVSA’s official crude production figure for 2013 was around 2.9 mbpd whereas the U.S. Energy Information Administration puts the figure at 2.5 mbpd. Despite the challenges of attaining reliable and consistent data about Venezuelan oil, the trends of declining overall production as well as declining exports to the United States—and conversely rising exports to China—are clear.