A mutation in the way companies are financed and managed will change the distribution of the wealth they create.

AT THE beginning of the 1980s capital was flooding into the American oil and gas industry. Apache Corporation, an erstwhile conglomerate spanning steel, dude-ranching and car sales, sought to tap into the flow in a novel way. It wrapped a bunch of private oil and gas assets into a new ownership structure that was akin to a partnership but was publicly listed. It was a useful idea—until steep declines in tax rates and energy prices put the Apache Petroleum Company to rest in 1987.

This time round the master limited partnership (MLP) structure which Apache pioneered is no longer just a footnote. In the 2000s such companies allowed the capital-intensive energy industry to attract vital funds even during a devastating financial crisis. Kinder Morgan, a complex entity built around interlocking MLPs, has an enterprise value (its market capitalisation plus its debt) of $109 billion. The collective market capitalisation of MLPs recently passed that of Exxon Mobil, the most highly valued energy company on the New York Stock Exchange.

The new popularity of the MLP is part of a larger shift in the way businesses structure themselves that is changing how American capitalism works. The essence is a move towards types of firm which retain very little of their earnings: “pass-through” companies which every year pay out more or less as much as they take in. Many of the standard rules that corporations which retain their earnings have to follow when dealing with shareholders do not apply to such firms. And, crucially, so long as they distribute their earnings such set-ups can largely avoid corporate tax.

Not all shall be partners

Mindful of that last point, the American government has in the past restricted the use of such structures. But these restrictions have eased, and more and more businesses are now twisting themselves into forms that allow them to qualify as pass-throughs. The corporation is becoming the distorporation.

Collectively, distorporations such as the MLPs have a valuation on American markets in excess of $1 trillion. They represent 9% of the number of listed companies and in 2012 they paid out 10% of the dividends; but they took in 28% of the equity raised. And these statistics underplay the true scale of the shift. Structures like MLPs are used to house the management of big private-equity companies, thus sitting atop industrial empires of much greater worth. Among all firms, in 2008 pass-through structures accounted for 23% of companies and 63% of profits, according to the latest data available from the Internal Revenue Service (IRS). Widely cited research by Rodney Chrisman, a professor at Liberty University School of Law, says such businesses account for more than two-thirds of new companies.

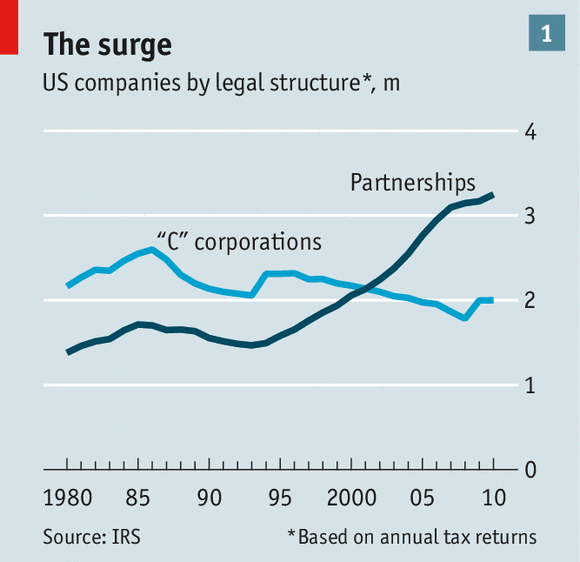

The shift to the distorporation comes at the expense of the “C” corporation, the formal name for the familiar limited-liability joint-stock structure that emerged a century ago (see chart 1). The newer structures still protect investors from liability. But the requirement for partnerships to pass through their money blocks the accumulation of earnings. In C corporations retained earnings can be used to fund investment and growth, assuring persistence. Without them, pass-through businesses have to be far more intertwined with investors. Staying alive means routinely inhaling capital, as well as exhaling.

These arrangements can be spectacularly lucrative for their general partner. Richard Kinder, who founded Kinder Morgan in 1997, now has a $9 billion stake, and received dividends of $376m over the past year. In a conventional C corporation shareholders might complain. In a complex set-up based around a pass-through entity, the views of the “limited partners”—investors—matter little. Their contracts give management a much freer hand than in familiar corporations, where government regulation grants shareholders a lot of rights. And those who invest in distorporations do pretty well out of the deal. Shareholders, or to be more precise “unit holders”, have received dividends double or triple the market average.

These beneficiaries, though, are a select class. Quirks in various investment and tax laws block or limit investing in pass-through structures by ordinary mutual funds, including the benchmark broad index funds, and by many institutions. The result is confusion and the exclusion of a large swathe of Americans from owning the companies hungriest for the capital the markets can provide, and thus from getting the best returns on offer.

This shift in how companies are governed and raise money is bringing with it a structural change in American capitalism. That should be a matter of great debate. Are these new businesses, with their ability to circumvent rules that apply to conventional public companies, merely adroit exploiters of loopholes for the benefit of a plutocratic few? Or do they reflect the adaptability on which America’s vitality has always been based? Alas, it is a debate the country is either blithely or studiously failing to take up.

Natural resources and unnatural acts

The move away from the C corporation began in earnest in 1975. Wyoming, that vibrant business hub, adopted a new entity structure, the limited-liability company (LLC). Imported from Panama, it provided the tax treatment of a partnership while preserving the corporate protection from individual liability for company debts and litigation. Other states followed in adopting the model. Businesses were quick to see the advantages.

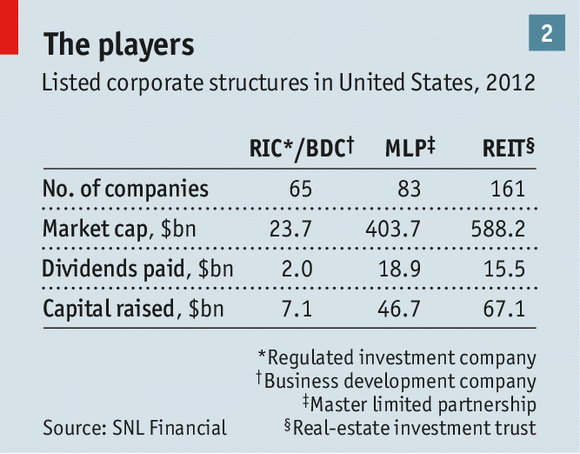

The various new types of firm that have risen in the wake of the LLC (see table 2) make similar use of partnership structures. They have tended to be industry- or sector-specific, at least to begin with. The energy business has a lot of MLPs not only because it needs capital but because it is an easy place to set them up: since 1987, tax law has allowed “mineral or natural resource” companies to operate as listed partnerships, while withholding that privilege from others. But as with other pass-through structures, the constraints are being lowered and circumvented.

For MLPs, the definition of “mineral or natural resource” is elastic. These days, for example, it is not just income from coal that qualifies; money made from rolling stock that carries coal on railways qualifies too. Allan Reiss, a lawyer at Morgan Lewis, notes that a year ago the IRS issued a ruling allowing the processing, storage, transport and marketing of olefins, a type of synthetic polymer, to be included as qualifying income. In 2007 private-equity firms seized on another clause in the tax law on interest and dividends that enabled the MLP structure to be used for publicly listed components of Apollo, Blackstone, Carlyle, KKR and other private-equity companies.

These days the limitations on becoming an MLP seem to be tied more to legal dexterity and influence than any underlying principle. Politicians want to extend the benefits of partnerships to industries they have come to favour either on the basis of ideology, or astute lobbying, or a bit of both. Sporadic interest in closing the loopholes companies use to twist themselves into such structures tends to sputter out, whether through genuine concern at the economic fallout or as a result of corporate emoluments spread over the appropriate constituencies. Meanwhile the regulatory burdens on C corporations that make people look for alternatives in the first place grow apace.

Another booming pass-through structure is that of the “business development company” (BDC). These firms raise public equity and debt much like a leveraged fund. As vehicles for investing in other companies, BDCs are regulated by a division of the Securities and Exchange Commission (SEC) which is considered particularly pernickety, and thus, other things being equal, to be avoided. Other things are not equal: the arrangement has virtues for managers, the public and investors.

Of more than 40 publicly traded BDCs, only seven are structured in a manner that truly resembles an ordinary corporation, with boards and conventional shareholder votes. What they all share is an ability to do bank-like business—lending to companies which need money—without bank-like regulatory compliance costs. Since the investors providing capital are not insured by the government as bank depositors are, BDCs are not pressured to invest in designated “low risk” areas such as government bonds. Instead they can focus on funding private enterprise, filling credit needs conventional banks now ignore.

The largest and oldest group of companies to have a similar structure are the real-estate investment trusts (REITs). In 1960 clever property owners who wanted access to the public’s capital managed to insert a provision into the Cigar Excise Tax Extension Act which purported to expand opportunities to small investors. The REITs thus created were initially used as ways of owning residential housing and office space; they now encompass casinos, hospitals and mobile-phone towers. As with other pass-through structures, companies that cannot distort themselves enough to meet the definitions can still get some of the benefits. The premises of Walmart and CVS, a chain of drug stores, are held by REITs, as are the headquarters of the New York Times; the paper sold them and leased them back in 2009.

Hurly Berle times

Andrew Morriss, of the University of Alabama law school, sees the shift as an entrepreneurial response to a century’s worth of governmental distortions made through taxation and regulation. At the heart of those actions were the ideas set down in “The Modern Corporation and Private Property”, a landmark 1932 study by Adolf Berle and Gardiner Means. As Berle, a member of Franklin Roosevelt’s “brain trust”, would later write, the shift of “two-thirds of the industrial wealth of the country from individual ownership to ownership by the large, publicly financed corporations vitally changes the lives of property owners, the lives of workers and

almost necessarily involves a new form of economic organisation of society.”

In the late 19th century industry had a voracious need for capital; it found it by listing shares publicly on exchanges. The problem with this, Berle observed, was that over time big successful corporations would come to finance themselves out of retained earnings and have little need for investor-supplied capital. So while the ownership structure provided liquidity for shareholders—they could easily exchange rights for cash—it did not give them the authority tied to conventional ownership, because the company did not need to maintain their support.

“Management thus becomes,” Berle wrote, “in an odd sort of way, the uncontrolled administrator of a kind of trust.” As these trusts became huge, it was inevitable that laws would be passed requiring them to use their wealth “more or less corresponding to the evolving expectations of American civilisation”. These included rules governing the treatment of employees and customers that went beyond what they might have been willing to enter into through private contracts, as well as rules which governed how management should treat owners. The SEC was established two years after the book by Berle and Means was published, and reflected just this sort of thinking.

Several minor retreats notwithstanding, the government’s role in the publicly listed company has expanded relentlessly ever since. Recent attempts by entrepreneurial legislators to exert more power over companies have, unsurprisingly, led to legal entrepreneurialism on the private side: hence the distorporation. As the move to new structures has picked up speed, from 1997 on, the number of companies with enough of a conventional structure—and trading volume—to be in Vanguard’s total market index fund has plunged from 7,306 in 1997 to 3,369 today.

The conventionally structured companies in this group are required to be ever more open to the wishes of their shareholders, with huge battles over such matters as compensation and the voting procedures for directors, work conditions and human rights, the virtues of which may not include higher returns. Meanwhile, an entire layer of public companies using these new structures stands outside the debate. The prospectuses that Apollo, Blackstone, Carlyle and KKR published before listing are clear about the rights of unit holders to influence corporate decisions: “limited” is an understatement.

This does not mean management is unconstrained. The requirement that most or all earnings must be returned means that investment capital must constantly be raised afresh. That means the financial markets are much more closely entangled with keeping these firms running, providing vast buckets of money when, as has been the case recently in energy, conditions are promising, and turning the taps off when they are not.

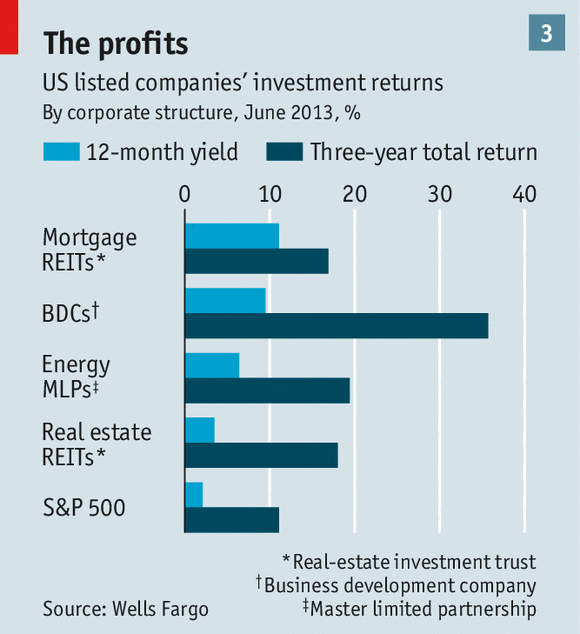

The relationship between owners and managers, however, has effectively been reduced to a single critical factor: the ability of these sorts of entities to pay out large distributions (see chart 3). Protection from corporation tax means that a pipsqueak MLP with a low credit rating can profitably acquire assets from established giants such as Chevron and Shell. For an oil or gas pipeline with a stable business, a common payout is 6%—extraordinarily high in the current environment when the average yield is 2%. For an exploration company, the payout could be in the mid-teens. Blackstone’s yield is 4%; KKR’s 8%. As in emerging markets without formal financial systems—where investors often lack principal protection, faith in accounting and confidence in government actions—investors make their choices purely on the consistency of payments.

Perhaps not surprisingly, one area where the structures have a particularly strong impact is on compensation. It typically follows either the hedge-fund model—based on assets, with a healthy slug of profits (20%) on top—or some sort of stepped arrangement, with the general partner receiving as much as 50% of the quarterly distributions as thresholds are reached. The full benefits of such partnerships can be remarkable. For a partner a payout can be considered merely a return of capital rather than a profit, and consequently no tax is due until the sale of the underlying security. When tied to nuances of estate law, this may mean no tax at all.

Breathing in, breathing out

For institutions such as endowments and sovereign wealth funds which themselves can be entirely or partially tax exempt, the issues tied to investing in these entities are formidably complex. They thus provide lucrative opportunities not only for people running companies but for accountants, lawyers, lobbyists, and those well versed in the state and local politics tied to the finer points of the tax code.

That is good for insiders but not so helpful for people trying to understand what is going on. The standard approach to security analysis, capital allocation and market valuation that begins with comparisons between companies’ returns using metrics such as price to earnings or book value becomes much less relevant, and possibly misleading, in such situations. There is, for example, much debate about Kinder Morgan’s true worth.

Because all these structures rest on special provisions and waivers of law, they survive on the whims of Washington. Their attempt to escape the reach of politically motivated changes in governance and taxation inevitably tends to hinge on lobbying and cronyism somewhere along the line. It is, in short, an example of how the system can be rigged to favour the connected. It may seem odd, then, that the shift has not produced more of an outcry.

In part, this is because its complexity shields it from scrutiny, and because, unlike politicians who seek to publicise their attempts to regulate business, business tends to keep quiet about its successful acts of resistance. But it is also because the questions it raises do not fit into the established world views of either the left or the right. The left typically responds to concerns about business with a belief in antitrust actions to break up size and with strengthened regulation. The conservative alternative has been to emphasise corporate governance, level playing fields and best practices. Neither approach offers much in this case.

But if the shift prompts genuine concerns, it is also specifically and broadly virtuous—because it enables capital to be channelled to where it can have a return, rather than sitting in the roach motel of retained earnings on which C corporations are based. That may, in the end, be the most compelling component of whatever defines the American system and enables it to be productive and innovative. For all the inequities, when vast wealth has been made through these structures, it has been in cases where the underlying assets produced more cash, not less.

fecha |

Título |

23/09/2023| |

|

06/09/2022| |

|

17/09/2020| |

|

15/09/2020| |

|

18/08/2020| |

|

05/07/2020| |

|

01/06/2020| |

|

30/05/2020| |

|

15/05/2020| |

|

26/04/2020| |

|

14/04/2020| |

|

04/04/2020| |

|

24/03/2020| |

|

19/01/2020| |

|

23/08/2019| |

|

22/08/2019| |

|

20/08/2019| |

|

21/07/2019| |

|

04/02/2019| |

|

13/01/2019| |

|

26/12/2018| |

|

24/12/2018| |

|

04/10/2018| |

|

13/08/2018| |

|

12/08/2018| |

|

07/08/2018| |

|

03/08/2018| |

|

28/07/2018| |

|

25/07/2018| |

|

23/07/2018| |

|

23/07/2018| |

|

21/07/2018| |

|

01/07/2018| |

|

12/06/2018| |

|

26/04/2018| |

|

22/04/2018| |

|

10/04/2018| |

|

24/03/2018| |

|

20/03/2018| |

|

04/03/2018| |

|

03/02/2018| |

|

11/12/2017| |

|

11/12/2017| |

|

11/12/2017| |

|

02/12/2017| |

|

17/11/2017| |

|

16/11/2017| |

|

07/11/2017| |

|

01/11/2017| |

|

28/10/2017| |

|

26/10/2017| |

|

05/10/2017| |

|

26/09/2017| |

|

09/09/2017| |

|

20/08/2017| |

|

19/08/2017| |

|

14/08/2017| |

|

01/08/2017| |

|

22/07/2017| |

|

20/07/2017| |

|

15/07/2017| |

|

09/07/2017| |

|

07/07/2017| |

|

12/06/2017| |

|

10/06/2017| |

|

13/05/2017| |

|

13/05/2017| |

|

30/04/2017| |

|

19/04/2017| |

|

18/04/2017| |

|

04/04/2017| |

|

28/03/2017| |

|

28/03/2017| |

|

17/03/2017| |

|

12/03/2017| |

|

05/03/2017| |

|

05/03/2017| |

|

24/02/2017| |

|

24/02/2017| |

|

22/02/2017| |

|

22/02/2017| |

|

20/02/2017| |

|

01/02/2017| |

|

16/01/2017| |

|

16/01/2017| |

|

15/01/2017| |

|

10/01/2017| |

|

01/01/2017| |

|

24/11/2016| |

|

20/11/2016| |

|

11/11/2016| |

|

24/10/2016| |

|

17/10/2016| |

|

15/10/2016| |

|

14/10/2016| |

|

14/10/2016| |

|

13/10/2016| |

|

10/10/2016| |

|

01/10/2016| |

|

14/09/2016| |

|

09/09/2016| |

|

04/09/2016| |

|

04/09/2016| |

|

17/08/2016| |

|

14/08/2016| |

|

14/08/2016| |

|

16/06/2016| |

|

11/06/2016| |

|

06/06/2016| |

|

06/06/2016| |

|

27/05/2016| |

|

07/05/2016| |

|

14/04/2016| |

|

14/04/2016| |

|

11/04/2016| |

|

11/04/2016| |

|

25/03/2016| |

|

18/03/2016| |

|

18/03/2016| |

|

18/03/2016| |

|

15/03/2016| |

|

15/03/2016| |

|

13/03/2016| |

|

08/02/2016| |

|

07/02/2016| |

|

24/01/2016| |

|

05/01/2016| |

|

04/01/2016| |

|

31/12/2015| |

|

16/12/2015| |

|

16/12/2015| |

|

11/12/2015| |

|

28/11/2015| |

|

21/11/2015| |

|

10/11/2015| |

|

07/11/2015| |

|

03/11/2015| |

|

31/10/2015| |

|

19/10/2015| |

|

19/10/2015| |

|

15/10/2015| |

|

28/09/2015| |

|

20/09/2015| |

|

18/09/2015| |

|

03/09/2015| |

|

31/08/2015| |

|

28/08/2015| |

|

21/08/2015| |

|

16/08/2015| |

|

08/08/2015| |

|

08/08/2015| |

|

30/07/2015| |

|

30/07/2015| |

|

22/07/2015| |

|

27/06/2015| |

|

27/06/2015| |

|

17/06/2015| |

|

09/06/2015| |

|

06/06/2015| |

|

03/06/2015| |

|

30/05/2015| |

|

30/05/2015| |

|

22/05/2015| |

|

21/05/2015| |

|

19/05/2015| |

|

06/05/2015| |

|

02/05/2015| |

|

03/04/2015| |

|

31/03/2015| |

|

29/03/2015| |

|

09/03/2015| |

|

04/03/2015| |

|

25/02/2015| |

|

19/02/2015| |

|

16/02/2015| |

|

16/02/2015| |

|

01/02/2015| |

|

01/02/2015| |

|

27/01/2015| |

|

27/01/2015| |

|

27/01/2015| |

|

23/01/2015| |

|

22/01/2015| |

|

13/01/2015| |

|

13/01/2015| |

|

02/01/2015| |

|

02/01/2015| |

|

22/12/2014| |

|

21/12/2014| |

|

21/12/2014| |

|

18/12/2014| |

|

14/12/2014| |

|

04/12/2014| |

|

01/12/2014| |

|

01/12/2014| |

|

28/11/2014| |

|

20/11/2014| |

|

20/11/2014| |

|

12/11/2014| |

|

01/11/2014| |

|

21/10/2014| |

|

19/10/2014| |

|

18/10/2014| |

|

14/10/2014| |

|

12/10/2014| |

|

12/10/2014| |

|

12/10/2014| |

|

10/10/2014| |

|

06/10/2014| |

|

06/10/2014| |

|

01/10/2014| |

|

29/09/2014| |

|

29/09/2014| |

|

19/09/2014| |

|

15/09/2014| |

|

09/09/2014| |

|

01/09/2014| |

|

26/08/2014| |

|

26/08/2014| |

|

19/08/2014| |

|

19/08/2014| |

|

08/08/2014| |

|

29/07/2014| |

|

29/07/2014| |

|

27/07/2014| |

|

27/07/2014| |

|

21/07/2014| |

|

21/07/2014| |

|

21/07/2014| |

|

03/07/2014| |

|

01/07/2014| |

|

23/06/2014| |

|

21/06/2014| |

|

18/06/2014| |

|

18/06/2014| |

|

18/06/2014| |

|

29/05/2014| |

|

21/05/2014| |

|

17/05/2014| |

|

09/05/2014| |

|

09/05/2014| |

|

09/05/2014| |

|

05/05/2014| |

|

27/04/2014| |

|

20/04/2014| |

|

20/04/2014| |

|

20/04/2014| |

|

11/04/2014| |

|

07/04/2014| |

|

31/03/2014| |

|

31/03/2014| |

|

25/03/2014| |

|

04/03/2014| |

|

27/02/2014| |

|

21/02/2014| |

|

17/02/2014| |

|

14/02/2014| |

|

04/02/2014| |

|

31/01/2014| |

|

31/01/2014| |

|

25/01/2014| |

|

16/01/2014| |

|

15/01/2014| |

|

15/01/2014| |

|

14/01/2014| |

|

02/01/2014| |

|

25/12/2013| |

|

19/12/2013| |

|

11/12/2013| |

|

11/12/2013| |

|

06/12/2013| |

|

03/12/2013| |

|

03/12/2013| |

|

27/11/2013| |

|

25/11/2013| |

|

20/11/2013| |

|

17/11/2013| |

|

11/11/2013| |

|

08/11/2013| |

|

06/11/2013| |

|

05/11/2013| |

|

28/10/2013| |

|

28/10/2013| |

|

27/10/2013| |

|

21/10/2013| |

|

21/10/2013| |

|

21/10/2013| |

|

16/10/2013| |

|

10/10/2013| |

|

09/10/2013| |

|

09/10/2013| |

|

29/09/2013| |

|

21/09/2013| |

|

17/09/2013| |

|

17/09/2013| |

|

15/09/2013| |

|

15/09/2013| |

|

14/09/2013| |

|

03/09/2013| |

|

27/08/2013| |

|

27/08/2013| |

|

17/08/2013| |

|

12/08/2013| |

|

12/08/2013| |

|

12/08/2013| |

|

07/08/2013| |

|

29/07/2013| |

|

18/07/2013| |

|

18/07/2013| |

|

12/07/2013| |

|

12/07/2013| |

|

11/07/2013| |

|

07/07/2013| |

|

06/07/2013| |

|

29/06/2013| |

|

21/06/2013| |

|

21/06/2013| |

|

16/06/2013| |

|

16/06/2013| |

|

16/06/2013| |

|

12/06/2013| |

|

03/06/2013| |

|

03/06/2013| |

|

30/05/2013| |

|

30/05/2013| |

|

28/05/2013| |

|

28/05/2013| |

|

28/05/2013| |

|

23/05/2013| |

|

23/05/2013| |

|

20/05/2013| |

|

20/05/2013| |

|

16/05/2013| |

|

16/05/2013| |

|

10/05/2013| |

|

10/05/2013| |

|

06/05/2013| |

|

04/05/2013| |

|

23/04/2013| |

|

21/04/2013| |

|

21/04/2013| |

|

19/04/2013| |

|

14/04/2013| |

|

11/04/2013| |

|

08/04/2013| |

|

03/04/2013| |

|

31/03/2013| |

|

22/03/2013| |

|

21/03/2013| |

|

14/03/2013| |

|

14/03/2013| |

|

11/03/2013| |

|

11/03/2013| |

|

11/03/2013| |

|

03/03/2013| |

|

03/03/2013| |

|

03/03/2013| |

|

03/03/2013| |

|

03/03/2013| |

|

25/02/2013| |

|

25/02/2013| |

|

18/02/2013| |

|

18/02/2013| |

|

18/02/2013| |

|

14/02/2013| |

|

14/02/2013| |

|

11/02/2013| |

|

11/02/2013| |

|

11/02/2013| |

|

27/01/2013| |

|

25/01/2013| |

|

22/01/2013| |

|

22/01/2013| |

|

15/01/2013| |

|

13/01/2013| |

|

10/01/2013| |

|

10/01/2013| |

|

10/01/2013| |

|

09/01/2013| |

|

09/01/2013| |

|

30/12/2012| |

|

25/12/2012| |

|

25/12/2012| |

|

24/12/2012| |

|

24/12/2012| |

|

19/12/2012| |

|

18/12/2012| |

|

18/12/2012| |

|

12/12/2012| |

|

08/12/2012| |

|

06/12/2012| |

|

05/12/2012| |

|

04/12/2012| |

|

04/12/2012| |

|

27/11/2012| |

|

26/11/2012| |

|

24/11/2012| |

|

24/11/2012| |

|

24/11/2012| |

|

19/11/2012| |

|

18/11/2012| |

|

18/11/2012| |

|

18/11/2012| |

|

10/11/2012| |

|

09/11/2012| |

|

09/11/2012| |

|

09/11/2012| |

|

07/11/2012| |

|

07/11/2012| |

|

07/11/2012| |

|

07/11/2012| |

|

07/11/2012| |

|

07/11/2012| |

|

05/11/2012| |

|

02/11/2012| |

|

02/11/2012| |

|

01/11/2012| |

|

31/10/2012| |

|

31/10/2012| |

|

30/10/2012| |

|

30/10/2012| |

|

26/10/2012| |

|

26/10/2012| |

|

26/10/2012| |

|

26/10/2012| |

|

19/10/2012| |

|

19/10/2012| |

|

19/10/2012| |

|

19/10/2012| |

|

19/10/2012| |

|

29/09/2012| |

|

10/09/2012| |

|

10/09/2012| |

|

10/09/2012| |

|

10/09/2012| |

|

10/09/2012| |

|

09/09/2012| |

|

01/09/2012| |

|

01/09/2012| |

|

01/09/2012| |

|

30/08/2012| |

|

24/08/2012| |

|

22/08/2012| |

|

22/08/2012| |

|

22/08/2012| |

|

21/08/2012| |

|

15/08/2012| |

|

15/08/2012| |

|

15/08/2012| |

|

13/08/2012| |

|

13/08/2012| |

|

10/08/2012| |

|

09/08/2012| |

|

09/08/2012| |

|

07/08/2012| |

|

06/08/2012| |

|

06/08/2012| |

|

06/08/2012| |

|

06/08/2012| |

|

31/07/2012| |

|

31/07/2012| |

|

31/07/2012| |

|

31/07/2012| |

|

28/07/2012| |

|

28/07/2012| |

|

28/07/2012| |

|

28/07/2012| |

|

28/07/2012| |

|

28/07/2012| |

|

28/07/2012| |

|

28/07/2012| |

|

25/07/2012| |

|

25/07/2012| |

|

15/07/2012| |

|

15/07/2012| |

|

14/07/2012| |

|

10/07/2012| |

|

10/07/2012| |

|

09/07/2012| |

|

14/06/2012| |

|

14/06/2012| |

|

09/06/2012| |

|

09/06/2012| |

|

09/06/2012| |

|

08/06/2012| |

|

04/06/2012| |

|

04/06/2012| |

|

03/06/2012| |

|

03/06/2012| |

|

21/05/2012| |

|

20/05/2012| |

|

20/05/2012| |

|

06/05/2012| |

|

27/04/2012| |

|

13/04/2012| |

|

13/04/2012| |

|

13/04/2012| |

|

12/04/2012| |

|

12/04/2012| |

|

07/04/2012| |

|

07/04/2012| |

|

06/04/2012| |

|

06/04/2012| |

|

04/04/2012| |

|

01/04/2012| |

|

01/04/2012| |

|

01/04/2012| |

|

19/03/2012| |

|

19/03/2012| |

|

18/03/2012| |

|

18/03/2012| |

|

12/03/2012| |

|

12/03/2012| |

|

04/03/2012| |

|

04/03/2012| |

|

04/03/2012| |

|

04/03/2012| |

|

04/03/2012| |

|

04/03/2012| |

|

04/03/2012| |

|

04/03/2012| |

|

02/03/2012| |

|

02/03/2012| |

|

02/03/2012| |

|

25/02/2012| |

|

25/02/2012| |

|

25/02/2012| |

|

25/02/2012| |

|

25/02/2012| |

|

25/02/2012| |

|

05/11/2011| |

|

30/10/2011| |

|

30/10/2011| |

|

29/10/2011| |

|

21/10/2011| |

|

11/10/2011| |

|

11/10/2011| |

|

08/10/2011| |

|

04/10/2011| |

|

03/10/2011| |

|

03/10/2011| |

|

03/10/2011| |

|

01/10/2011| |

|

01/10/2011| |

|

25/09/2011| |

|

24/09/2011| |

|

23/09/2011| |

|

23/09/2011| |

|

23/09/2011| |

|

23/09/2011| |

|

23/09/2011| |

|

20/09/2011| |

|

17/09/2011| |

|

17/09/2011| |

|

16/09/2011| |

|

15/09/2011| |

|

11/09/2011| |

|

11/09/2011| |

|

07/09/2011| |

|

07/09/2011| |

|

04/09/2011| |

|

04/09/2011| |

|

04/09/2011| |

|

04/09/2011| |

|

02/09/2011| |

|

02/09/2011| |

|

02/09/2011| |

|

02/09/2011| |

|

27/08/2011| |

|

27/08/2011| |

|

27/08/2011| |

|

27/08/2011| |

|

26/08/2011| |

|

26/08/2011| |

|

26/08/2011| |

|

26/08/2011| |

|

25/08/2011| |

|

25/08/2011| |

|

23/08/2011| |

|

23/08/2011| |

|

16/08/2011| |

|

16/08/2011| |

|

16/08/2011| |

|

16/08/2011| |

|

11/08/2011| |

|

11/08/2011| |

|

11/08/2011| |

|

07/08/2011| |

|

04/08/2011| |

|

29/07/2011| |

|

28/07/2011| |

|

24/07/2011| |

|

24/07/2011| |

|

23/07/2011| |

|

23/07/2011| |

|

22/07/2011| |

|

21/07/2011| |

|

21/07/2011| |

|

17/07/2011| |

|

17/07/2011| |

|

15/07/2011| |

|

15/07/2011| |

|

15/07/2011| |

|

15/07/2011| |

|

13/07/2011| |

|

13/07/2011| |

|

13/07/2011| |

|

13/07/2011| |

|

29/06/2011| |

|

29/06/2011| |

|

19/06/2011| |

|

19/06/2011| |

|

19/06/2011| |

|

19/06/2011| |

|

18/06/2011| |

|

18/06/2011| |

|

18/06/2011| |

|

18/06/2011| |

|

17/06/2011| |

|

17/06/2011| |

|

14/06/2011| |

|

14/06/2011| |

|

13/06/2011| |

|

13/06/2011| |

|

13/06/2011| |

|

13/06/2011| |

|

05/06/2011| |

|

05/06/2011| |

|

03/06/2011| |

|

03/06/2011| |

|

03/06/2011| |

|

03/06/2011| |

|

01/06/2011| |

|

01/06/2011| |

|

01/06/2011| |

|

01/06/2011| |

|

01/06/2011| |

|

01/06/2011| |

|

01/06/2011| |

|

01/06/2011| |

|

29/05/2011| |

|

29/05/2011| |

|

29/05/2011| |

|

29/05/2011| |

|

29/05/2011| |

|

29/05/2011| |

|

23/05/2011| |

|

23/05/2011| |

|

22/05/2011| |

|

22/05/2011| |

|

22/05/2011| |

|

22/05/2011| |

|

22/05/2011| |

|

22/05/2011| |

|

21/05/2011| |

|

21/05/2011| |

|

21/05/2011| |

|

21/05/2011| |

|

16/05/2011| |

|

16/05/2011| |

|

13/05/2011| |

|

13/05/2011| |

|

06/05/2011| |

|

06/05/2011| |

|

04/05/2011| |

|

04/05/2011| |

|

04/05/2011| |

|

04/05/2011| |

|

02/05/2011| |

|

02/05/2011| |

|

02/05/2011| |

|

02/05/2011| |

|

01/05/2011| |

|

01/05/2011| |

|

01/05/2011| |

|

01/05/2011| |

|

01/05/2011| |

|

01/05/2011| |

|

26/04/2011| |

|

26/04/2011| |

|

26/04/2011| |

|

26/04/2011| |

|

26/04/2011| |

|

26/04/2011| |

|

21/04/2011| |

|

21/04/2011| |

|

21/04/2011| |

|

21/04/2011| |

|

20/04/2011| |

|

20/04/2011| |

|

20/04/2011| |

|

20/04/2011| |

|

20/04/2011| |

|

20/04/2011| |

|

15/04/2011| |

|

11/04/2011| |

|

11/04/2011| |

|

08/04/2011| |

|

03/04/2011| |

|

27/03/2011| |

|

27/03/2011| |

|

26/03/2011| |

|

26/03/2011| |

|

20/03/2011| |

|

20/03/2011| |

|

19/03/2011| |

|

19/03/2011| |

|

19/03/2011| |

|

13/03/2011| |

|

13/03/2011| |

|

12/03/2011| |

|

11/03/2011| |

|

11/03/2011| |

|

09/03/2011| |

|

07/03/2011| |

|

07/03/2011| |

|

05/03/2011| |

|

04/03/2011| |

|

04/03/2011| |

|

04/03/2011| |

|

18/02/2011| |

|

21/01/2011| |

|

21/01/2011| |

|

16/01/2011| |

|

16/01/2011| |

|

11/01/2011| |

|

08/01/2011| |

|

02/01/2011| |

|

02/01/2011| |

|

29/12/2010| |

|

29/12/2010| |

|

28/12/2010| |

|

26/12/2010| |

|

13/12/2010| |

|

13/12/2010| |

|

08/12/2010| |

|

02/12/2010| |

|

30/11/2010| |

|

30/11/2010| |

|

28/11/2010| |

|

26/11/2010| |

|

26/11/2010| |

|

24/11/2010| |

|

16/11/2010| |

|

16/11/2010| |

|

16/11/2010| |

|

09/11/2010| |

|

07/11/2010| |

|

31/10/2010| |

|

31/10/2010| |

|

31/10/2010| |

|

26/10/2010| |

|

25/10/2010| |

|

22/10/2010| |

|

18/10/2010| |

|

16/10/2010| |

|

16/10/2010| |

|

11/10/2010| |

|

10/10/2010| |

|

10/10/2010| |

|

09/10/2010| |

|

05/10/2010| |

|

28/09/2010| |

|

28/09/2010| |

|

24/09/2010| |

|

24/09/2010| |

|

22/09/2010| |

|

22/09/2010| |

|

15/09/2010| |

|

15/09/2010| |

|

15/09/2010| |

|

12/09/2010| |

|

12/09/2010| |

|

12/09/2010| |

|

12/09/2010| |

|

06/09/2010| |

|

06/09/2010| |

|

05/09/2010| |

|

05/09/2010| |

|

29/08/2010| |

|

29/08/2010| |

|

29/08/2010| |

|

29/08/2010| |

|

22/08/2010| |

|

22/08/2010| |

|

21/08/2010| |

|

21/08/2010| |

|

21/08/2010| |

|

21/08/2010| |

|

21/08/2010| |

|

21/08/2010| |

|

14/08/2010| |

|

13/08/2010| |

|

13/08/2010| |

|

07/08/2010| |

|

07/08/2010| |

|

12/07/2010| |

|

12/06/2010| |

|

12/06/2010| |

|

12/06/2010| |

|

24/05/2010| |

|

24/05/2010| |

|

11/05/2010| |

|

10/05/2010| |

|

09/05/2010| |

|

09/05/2010| |

|

09/05/2010| |

|

01/04/2010| |

|

01/04/2010| |

|

31/03/2010| |

|

31/03/2010| |

|

31/03/2010| |

|

28/03/2010| |

|

28/03/2010| |

|

28/03/2010| |

|

20/03/2010| |

|

12/03/2010| |

|

12/03/2010| |

|

12/03/2010| |

|

08/03/2010| |

|

07/03/2010| |

|

06/03/2010| |

|

05/03/2010| |

|

03/03/2010| |

|

03/03/2010| |

|

28/02/2010| |

|

21/02/2010| |

|

19/02/2010| |

|

14/02/2010| |

|

11/02/2010| |

|

11/02/2010| |

|

10/02/2010| |

|

08/02/2010| |

|

08/02/2010| |

|

08/02/2010| |

|

28/01/2010| |

|

25/01/2010| |

|

20/01/2010| |

|

20/01/2010| |

|

16/01/2010| |

|

16/01/2010| |

|

15/01/2010| |

|

15/01/2010| |

|

11/01/2010| |

|

11/01/2010| |

|

10/01/2010| |

|

07/01/2010| |

|

03/01/2010| |

|

03/01/2010| |

|

03/01/2010| |

|

17/12/2009| |

|

15/12/2009| |

|

15/12/2009| |

|

13/12/2009| |

|

13/12/2009| |

|

28/11/2009| |

|

28/11/2009| |

|

28/11/2009| |

|

28/11/2009| |

|

27/11/2009| |

|

27/11/2009| |

|

27/11/2009| |

|

27/11/2009| |

|

27/11/2009| |

|

27/11/2009| |

|

21/11/2009| |

|

21/11/2009| |

|

18/11/2009| |

|

18/11/2009| |

|

16/11/2009| |

|

16/11/2009| |

|

30/10/2009| |

|

30/10/2009| |

|

11/10/2009| |

|

10/10/2009| |

|

10/10/2009| |

|

07/10/2009| |

|

07/10/2009| |

|

04/10/2009| |

|

30/09/2009| |

|

30/09/2009| |

|

27/09/2009| |

|

27/09/2009| |

|

27/09/2009| |

|

22/09/2009| |

|

20/09/2009| |

|

18/09/2009| |

|

18/09/2009| |

|

18/09/2009| |

|

16/09/2009| |

|

16/09/2009| |

|

16/09/2009| |

|

08/09/2009| |

|

07/09/2009| |

|

06/09/2009| |

|

06/09/2009| |

|

05/09/2009| |

|

05/09/2009| |

|

26/08/2009| |

|

21/08/2009| |

|

19/08/2009| |

|

19/08/2009| |

|

15/08/2009| |

|

15/08/2009| |

|

15/08/2009| |

|

11/08/2009| |

|

11/08/2009| |

|

11/08/2009| |

|

11/08/2009| |

|

19/07/2009| |

|

19/07/2009| |

|

18/07/2009| |

|

18/07/2009| |

|

27/03/2009| |

|

22/03/2009| |

|

22/03/2009| |

|

27/01/2009| |

|

27/01/2009| |

|

27/01/2009| |

|

17/01/2009| |

|

17/01/2009| |

|

17/01/2009| |

|

17/01/2009| |

|

17/01/2009| |

|

17/01/2009| |

|

11/01/2009| |

|

06/12/2008| |

|

06/12/2008| |

|

06/12/2008| |

|

06/12/2008| |

|

23/11/2008| |

|

23/11/2008| |

|

16/11/2008| |

|

16/11/2008| |

|

04/11/2008| |

|

04/11/2008| |

|

03/11/2008| |

|

03/11/2008| |

|

24/10/2008| |

|

24/10/2008| |

|

24/10/2008| |

|

24/10/2008| |

|

15/09/2008| |

|

15/09/2008| |

|

15/09/2008| |

|

15/09/2008| |

|

15/09/2008| |

|

15/09/2008| |

|

06/09/2008| |

|

06/09/2008| |

|

05/09/2008| |

|

05/09/2008| |

|

05/09/2008| |

|

05/09/2008| |

|

01/09/2008| |

|

01/09/2008| |

|

01/09/2008| |

|

01/09/2008| |

|

22/08/2008| |

|

22/08/2008| |

|

17/08/2008| |

|

17/08/2008| |

|

16/08/2008| |

|

16/08/2008| |

|

28/07/2008| |

|

28/07/2008| |

|

28/07/2008| |

|

28/07/2008| |

|

28/07/2008| |

|

28/07/2008| |

|

19/07/2008| |

|

19/07/2008| |

|

24/05/2008| |

|

24/05/2008| |

|

03/05/2008| |

|

03/05/2008| |

|

29/04/2008| |

|

11/02/2008| |

|

05/01/2008| |

|

09/12/2007| |

|

18/11/2007| |

|

10/11/2007| |

|

10/11/2007| |

|

06/11/2007| |

|

06/11/2007| |

|

06/09/2007| |

|

26/08/2007| |

|

25/08/2007| |

|

11/07/2007| |

|

16/06/2007| |

|

16/06/2007| |

|

10/06/2007| |

|

10/06/2007| |

|

19/05/2007| |

|

19/05/2007| |

|

19/05/2007| |

|

19/05/2007| |

|

24/04/2007| |

|

24/04/2007| |

|

14/04/2007| |

|

14/04/2007| |

|

05/04/2007| |

|

05/04/2007| |

|

05/04/2007| |

|

28/02/2007| |

|

28/02/2007| |

|

05/02/2007| |

|

05/02/2007| |

|

04/02/2007| |

|

04/02/2007| |

|

04/02/2007| |

|

04/02/2007| |

|

04/02/2007| |

|

04/02/2007| |

|

29/01/2007| |

|

29/01/2007| |

|

29/01/2007| |

|

29/01/2007| |

|

11/01/2007| |

|

11/01/2007| |

|

11/01/2007| |

|

11/01/2007| |

|

27/12/2006| |

|

27/12/2006| |

|

27/12/2006| |

|

27/12/2006| |

|

27/12/2006| |

|

27/12/2006| |

|

20/12/2006| |

|

20/12/2006| |

|

17/11/2006| |

|

30/09/2006| |

|

28/07/2006| |

|

12/04/2006| |

|

12/04/2006| |

|

12/04/2006| |

|

06/03/2006| |

|

21/02/2006| |

|

17/02/2006| |

|

31/01/2006| |

|

10/01/2006| |

|

28/12/2005| |

|

31/10/2005| |

|

26/09/2005| |

|

29/08/2005| |

|

11/08/2005| |

|

08/08/2005| |

|

24/06/2005| |

|

24/06/2005| |

|

24/06/2005| |

|

03/04/2005| |

|

03/04/2005| |

|

03/04/2005| |

|

03/04/2005| |

|